Calculating Budgeted Hourly Rates (BHR)

For Printing and Packaging Organizations

An essential tool for being a competitive and profitable printing organization is budgeted hourly rates (BHRs). Budgeted hourly rates distribute 100 percent of an organization’s expenses

among each piece of production equipment so that all costs are fully absorbed and accounted for in estimates, price quotes, and job costs. Accurate BHRs which reflects true out-of-pocket costs help

printing organizations intelligently and competitively price jobs.

An essential tool for being a competitive and profitable printing organization is budgeted hourly rates (BHRs). Budgeted hourly rates distribute 100 percent of an organization’s expenses

among each piece of production equipment so that all costs are fully absorbed and accounted for in estimates, price quotes, and job costs. Accurate BHRs which reflects true out-of-pocket costs help

printing organizations intelligently and competitively price jobs.

- Determine the cost per hour to operate a piece of production equipment or cost center

- Based on annual expenses (cost of doing business) and billable plant productivity

- Used to recover out-of-pocket costs, estimate costs, forecast profitability, determine prices, and measure performance

- Does not include job related consumables typically charged separately (paper, ink, film, plates, packing materials, etc.)

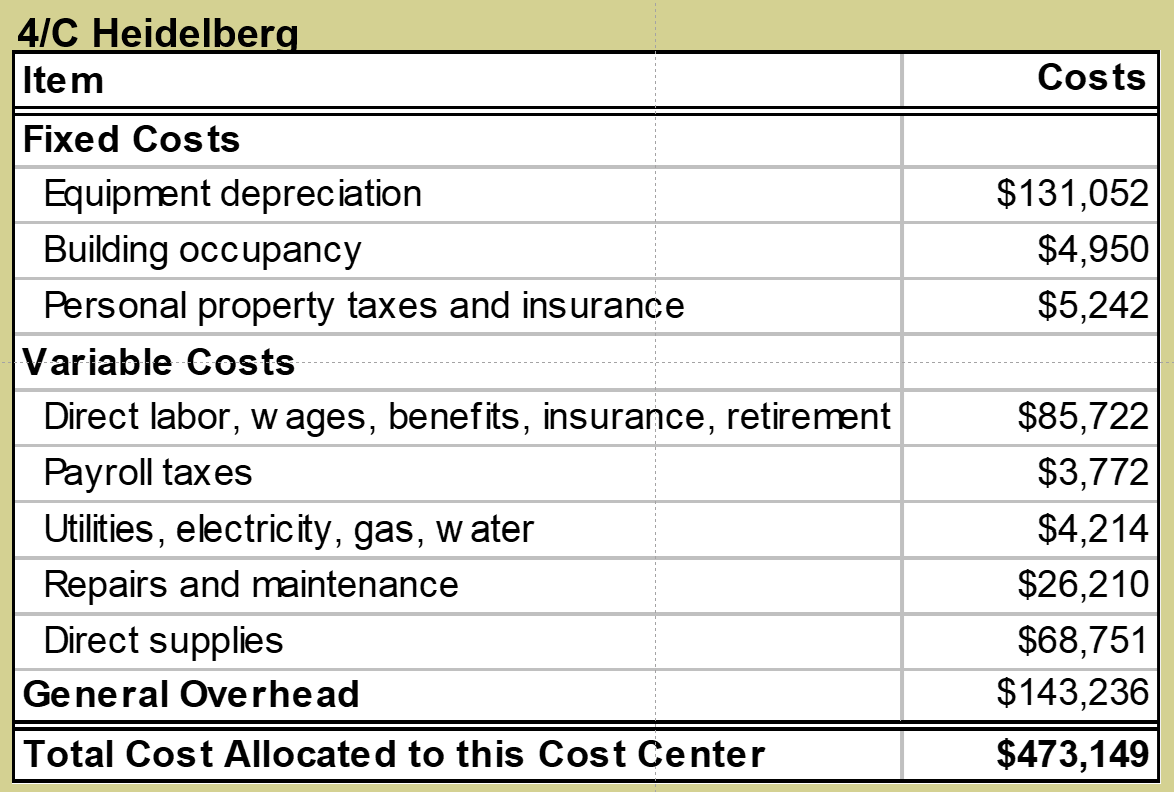

BHRs are comprised of direct and indirect costs including wages and benefits, building costs, leases, equipment depreciation, repairs and maintenance, utilities, insurance, office supplies, production supplies, sales expenses, and other costs. These costs are then distributed among each piece of equipment using various formulas and accounting principles.

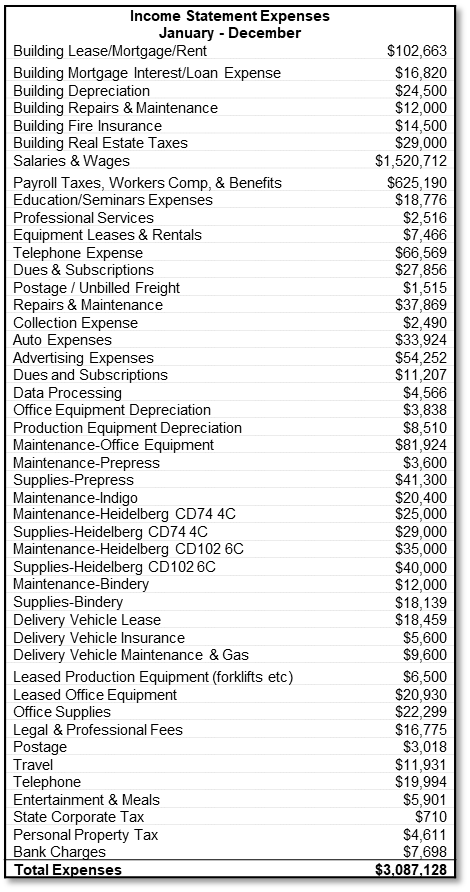

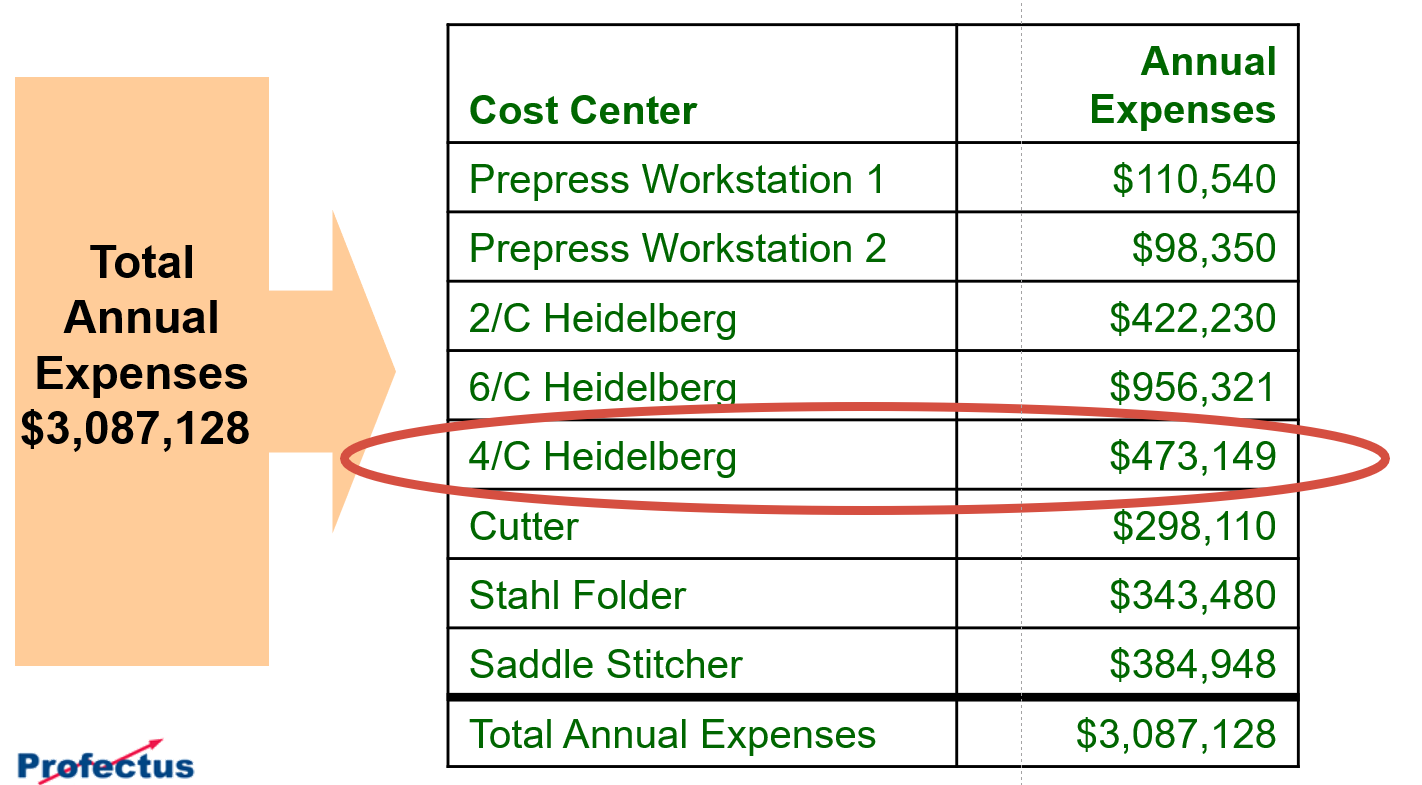

Expenses Component

- Annual expenses are the foundation for establishing BHRs

- Most predicable figures of the BHRs formula

- Expenses come right from your income statement or annual budget

- The main objective for implementing BHRs is to recover 100% of all your expenses

100% of the expenses are distributed among each cost centers proportionately based on the cost center’s direct expenses

Equipment Depreciation Expenses

- Depreciation based on the original investment

- Even when equipment is fully depreciated, the industry practice is that you keep depreciating it

- based either on the original investment cost or on a reasonable replacement cost

- The machine will need replacement at some time, and you do not want to pass that cost on to the customer

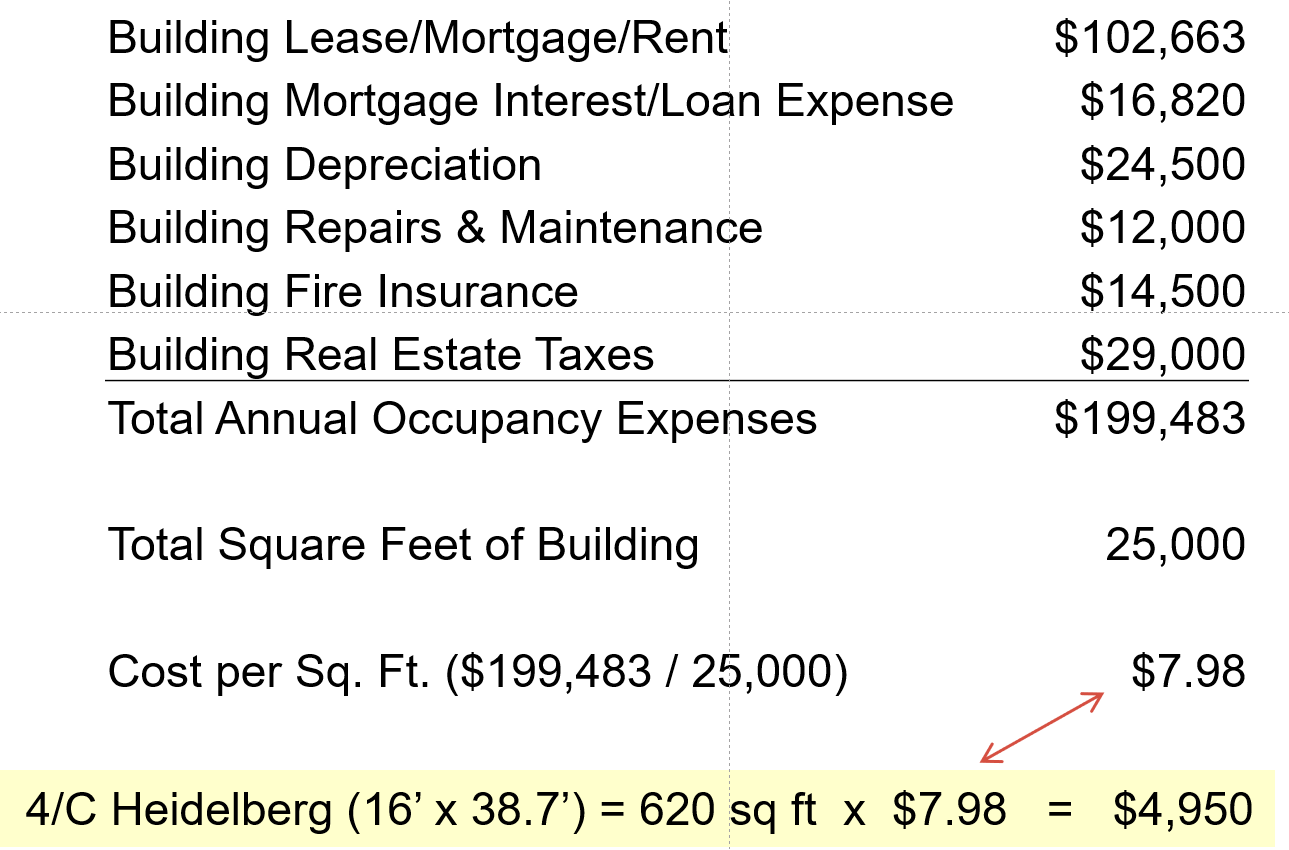

Building Occupancy Expenses

The building and occupancy cost component of a cost center's BHR is based on the cost per square foot and the area (in square feet) occupied by cost center.

First, add up all of the building and occupancy expenses and divided the total expenses by the total square feet of your building or facility.

Next, get the square footage of each cost center, measure the length and width of the working area of each cost center or machine. Be sure to include the immediate areas required to work on the machine such as the staging area delivery areas. The balance of the building area (aisles, common areas, offices, etc) will become overhead.

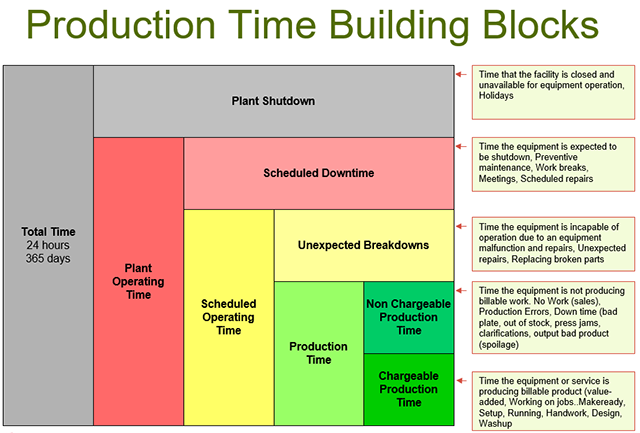

Equipment Productivity

The ratio of production hours charged to jobs to the available capacity

Total hours charged to jobs

÷ Total available hours

= % productive or % chargeable hours

The industry goal is approximately 85% productivity

What influences productivity?

Productive Time - Equipment is producing billable work

- Makeready, running, washups, customer OK’s

Non-Productive Time - equipment is not producing billable work

- No work due to lack of sales

- Production errors causing downtime - bad plate, out of stock, press jams, clarifications

- Output of bad product, spoilage

- Inefficient Scheduling

- Repairs, maintenance, meetings

Annual expenses are then recovered by the production hours you sell to customers or "Chargeable Hours". Chargeable production hours is when equipment is producing billable work Makeready, running, washups, customer OK’s.

BHRs typically do not include job related consumables such as paper, ink, plates, packing materials, or outside services. These costs are usually estimated and charged separately.

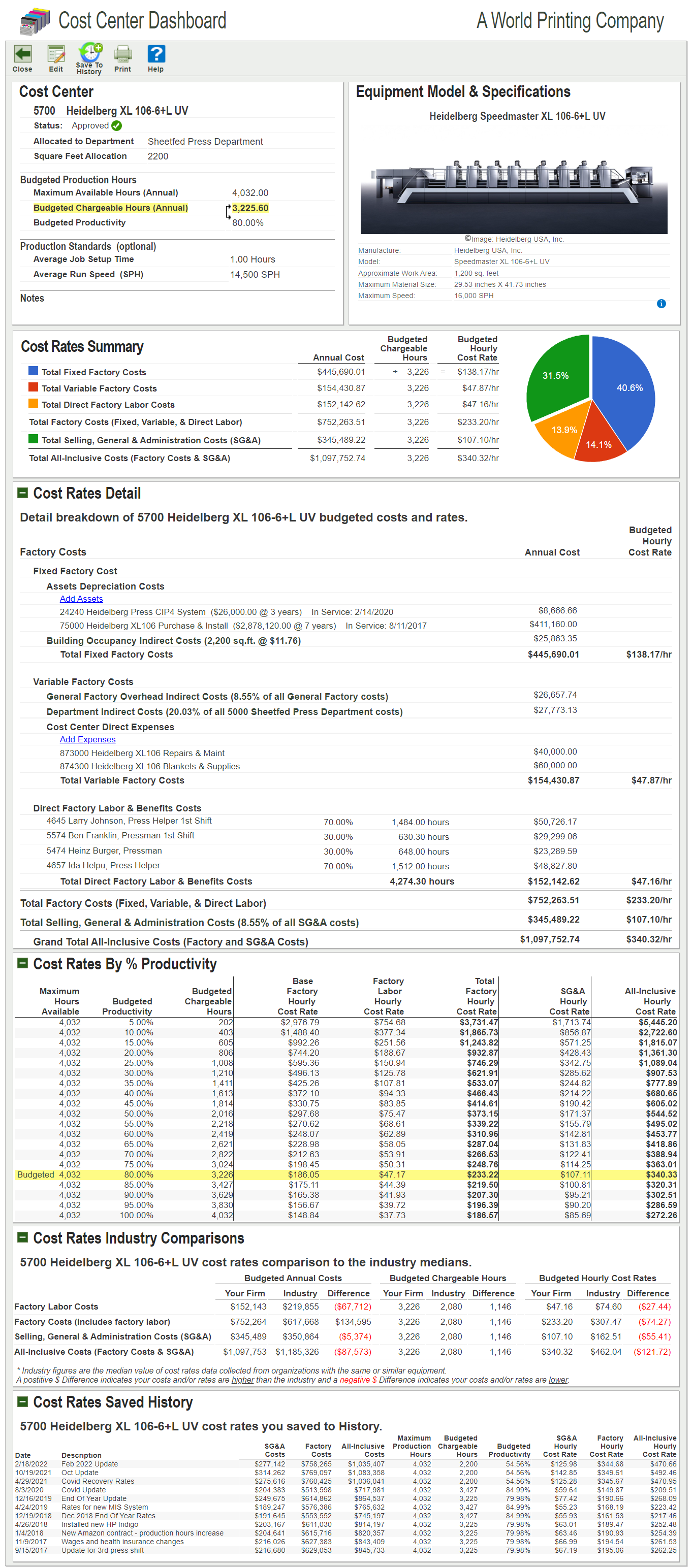

Companies can calculate their budgeted hourly rates using spreadsheets or BHR software such as the Cost Rates Advisor www.costratesadvisor.com An organization should update their BHRs at least annually or anytime there are significant cost changes including equipment purchases, wage increases, personnel changes, increases or decreases in revenues, or other major cost fluctuations.

Maintaining current BHRs enables organizations to be more competitive on the desirable and profitable work, and avoids the less lucrative work.

If your organization has not updated your BHRs in the last year, you could be losing profits and missing out on the more lucrative higher margin quotes.

More information about Calculating Budgeted Hourly Rates.

By: Craig L Press, President, Profectus Inc.